The Bidding War: How Sequoia's Whisper Campaign Led to A $19 Billion WhatsApp Buyout

Day 5 of the FTC trial rounded out the WhatsApp story, taking us through an admitted rumor, a timely run-in that leaked a Google meeting, and some very rich VCs.

Today at Big Tech on Trial, we have a double feature for you. Matt Stoller covered the first day of the Google Search remedy phase; you can read that in-depth account here. Down the hall, I covered the fifth day of FTC v. Meta Platforms. Read on for that summary below.

The deal that joined Facebook and WhatsApp came together in earnest in Mark Zuckerberg’s home on Valentine’s Day 2014. As we learned in court today, it almost didn’t come together at all. Things kicked into high gear when Facebook learned of a planned meeting between WhatsApp’s co-founders with Google co-founder Larry Page and his would-be successor as CEO, Sundar Pichai. What followed was a mad dash by Zuckerberg not to let WhatsApp get away. $19 billion later, he got his prize. 11 years after that, the combined company is on trial for it.

The whirlwind story of how Facebook acquired WhatsApp came into clearer view during Day 5 of the FTC’s trial to unwind that deal. We are seeing the same deal through the eyes of most of the principals, Rashomon-style: last week, from Meta founder Mark Zuckerberg and former COO Sheryl Sandberg, plus Jim Goetz of Sequoia Capital; and today, from WhatsApp Chief Business Officer Neeraj Arora and former Meta Vice President of Corporate Development Amin Zoufonoun (by video). The day started with the FTC’s expert, Jihoon Rim—himself the founder of rival chat platform, Kakao, and the inspiration (so the FTC says) for Zuckerberg’s relentless pursuit of WhatsApp. We also heard from Goetz’s partner, Roelof Botha (also by video), who led Sequoia’s investment in Instagram.

I’ve summarized today in narrative form, rather than by witness, citing them as appropriate. This WhatsApp chronology also draws on the prior reporting by Parmy Olson of Forbes that came up in court today.

“Get Together?”

In the spring of 2012, Zuckerberg emailed WhatsApp founder Jan Koum to invite him over to dinner with the subject line, “Get together?”, as reported by Forbes. At the time, WhatsApp was backed by Sequoia Capital, the legendary Silicon Valley venture capital firm that over the years had invested in Apple, Cisco, and YouTube. Koum demurred, eventually forwarding the chain to his contact at Sequoia, Jim Goetz. “Persistent!” Goetz wrote.

The two co-founders would soon meet at Esther’s German Bakery, with Zuckerberg dropping hints about working together. Koum summarized a 2012 meeting with Zuckerberg to Goetz:

"yeah talked about WeChat with Zuck on Sunday at length. he was actually very concerned Tencent was trying to buy us to compete with FB outside of china".

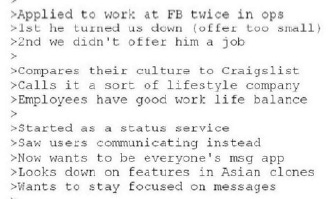

And we have Zuckerberg’s notes from a 2012 meeting, too, which he circulated to Facebook executives including Amin Zoufonoun. Those notes show something Meta is trying to show at trial, that WhatsApp wanted “to stay focused on messages” rather than expand into being a social network:

All in all, Zuckerberg called Koum “fairly impressive although disappointingly (or maybe positively for us) unambitious.” But the interest was there. In January 2013, Zuckerberg told Facebook’s board of directors that the “biggest competitive vector for us” was the possibility that a messaging app could transform “into a broader social network”:

A few months later, in April 2013, a rumor was circulating that Google was going to buy WhatsApp for $1 billion:

Zuckerberg emailed the story to Jan Koum, adding, “If you are thinking of having WhatsApp join another company, we’d of course love to talk at this price range and are almost certainly a much better fit than Google!” Koum denied it, replying that they “[w]ould never sell for such a low price - it is almost insulting of these tech reporters to value us so low . . . idiots.” Zuck wouldn’t be deterred, writing back asking if Koum would sell for more:

Behind the scenes, Jim Goetz was advising Koum to “avoid the lunch” because “you could get tencent, facebook and google into a bidding war (with microsoft and yahoo trailing)”. That made me wonder—who was behind the “rumor” of a Google acquisition anyway? And had the bidding war already started?

"It wasn't like there was dinner and candlelight”

Before he became the de facto chief business officer at WhatsApp, Neeraj Arora, the FTC’s second witness of the day, worked at Google. In the 2010-2011 timeframe, he made an offer on behalf of Google to acquire WhatsApp, and the parties negotiated on price. Google eventually upped its offer to close to $100 million. In an internal Google pitch deck we saw today, the “Strategic Rationale” was, in part, to “[o]btain an extremely viral product that works across all smartphone platforms, potentially grow it into a mobile social network”.

Through that process, Arora got to know WhatsApp’s founders, Koum and Brian Acton, and then left Google to join WhatsApp to head the business function. In one exhibit, Sequoia’s Goetz writes Arora, saying that they “should discuss all the inbound M&A interest we received over the last three days,” citing Twitter, Tencent, Microsoft, Google, Yahoo, Facebook, Quattrone and Grimes. (Quattrone is likely a reference to tech investor Frank Quattrone of Qatalyst Partners.)

And Grimes, Arora said, was a reference to Michael Grimes, then of Morgan Stanley, which, we learned through the FTC’s expert, was cozying up to WhatsApp to become their M&A adviser in early 2014. As Morgan Stanley saw it, “Google’s resources combined with WhatsApp’s user base and traction could create the preeminent social network on mobile (surpassing Facebook).” In a part of the email that was redacted, but read aloud anyway, Arora notes that Marissa Mayer had pinged him separately, who had likely by then left Google to become CEO of Yahoo!. The FTC had asked about other buyout offers WhatsApp was receiving, either through Sequoia or elsewhere; but Arora testified that they were “not real offers,” citing Tencent and Facebook as potential legitimate bidders.

By all accounts, WhatsApp’s founders were idealistic. Acton kept a signed note, still proudly displayed on Sequoia’s website, that read: “No Ads! No Games! No Gimmicks!” Goetz and Arora both testified that WhatsApp’s founders did not want to introduce advertising to their mobile messaging app, which had moved to a freemium model: the first year free, followed by a $1 annual subscription. Rim, the FTC’s expert—with some experience of his own monetizing a mobile messaging app—testified in response to questioning from Chief Judge Boasberg that the subscription model probably would not be successful given that carriers were reducing SMS text messaging costs to $0, including unlimited free texts in mobile phone plans. At the same time, the carriers were slow to implement what’s known as “direct carrier billing,” which allows subscribers to buy a paid app like WhatsApp with their phone bill. Goetz called the idea that he could “force” Koum and Acton to add advertising instead as “laughable” notwithstanding Sequoia’s investment. And his brag sheet on the Sequoia website seems to praise the co-founders’ approach, even citing Koum’s childhood experience with totalitarian communist rule as inspiration for it:

“When we first partnered with WhatsApp in January 2011, it had more than a dozen direct competitors, and all were supported by advertising. . . Jan and Brian ignored conventional wisdom. Rather than target users with ads – an approach they had grown to dislike during their time at Yahoo – they chose the opposite tack and charged a dollar for a product that is based on knowing as little about you as possible. . . . It’s a decidedly contrarian approach shaped by Jan’s experience growing up in a communist country with a secret police.”

And yet, the valuation analysis Sequoia would perform for potential investors in WhatsApp was premised on WhatsApp monetizing ads, not selling subscriptions: it used Facebook as a comparable to reach high valuations in the range of a 20x-25x multiple of EBITDA (earnings before interest, taxes, depreciation, and amortization). Facebook, internally, did likewise. Nobody seemed to think the valuation of WhatsApp should be tied to the co-founders’ own preference not to have ads.

While the future looked bright, the status quo was less rosy. WhatsApp had come back to Sequoia for more funding rounds; one task was the planned expansion of WhatsApp’s web-based client. At the same time, it was hemorrhaging cash; the FTC’s expert, Rim, testified that WhatsApp had more than $130 million in costs against $10 million in revenue in 2013. Faced with the obvious, the founders would have to accept some monetization, Rim explained. In the end, they chose to sell.

Fast forward to February 2014. A WhatsApp staffer “ran into” Facebook’s head of business development, Amin Zoufonoun, on Friday, February 7, and let drop that Koum had a meeting planned the next week with Google’s Page and Pichai. We heard about 11 minutes of testimony from Zoufonoun, who confirmed that while there was a difference of opinion within Facebook, some worried that WhatsApp might be a “Trojan horse wedge” that would pivot to social networking.

Zoufonoun got the process going, looping in Zuckerberg, who invited Koum to his house that Sunday night; Forbes reported they met Monday night. In Arora’s telling, Zuckerberg suggested a “partnership” with WhatsApp where Koum would join Facebook’s board and WhatsApp would operate independently.

The next day, Koum and Acton met with Page and Pichai at Google’s Mountainview, California campus. Per the reporter’s notes for the Forbes story, which she shared with Arora, WhatsApp was now valuing itself at $20 billion or more, based on the then-market capitalization of Twitter, the user base, and “future monetization.” Page didn’t make any offer. And by that point, it seemed clear that WhatsApp was ready to dance with Facebook.

Koum and Acton had dinner at Zuckerberg’s home two days later. They started negotiating on price. Koum came by again Friday, denying that he interrupted the Zuckerberg-Chan Valentine’s Day; as Forbes quoted him, “It wasn't like there was dinner and candlelight and I barged in through the door." By Saturday night, they had an agreement in principle: $19 billion for WhatsApp, plus a pledge that would keep its independence and give Koum a board seat. Koum and Zuckerberg celebrated with a bottle of Johnnie Walker Blue, per Forbes.

By that point, Arora came in to help “paper” the deal over. Zoufonoun wanted WhatsApp to agree to a no-shop clause, a fairly common deal protection device in M&A, but one the FTC will use to show that Facebook was concerned about others making a topping bid to take WhatsApp.

By the 17th, Facebook had what appeared to be a Board recommendation to do the deal. But it seemed to rely on advertising in projecting that WhatsApp could reach $1 billion in revenue:

The deal had some unique features that seemed to anticipate antitrust regulatory problems. The Facebook deck’s final two bullets admitted that there “[c]ould be a significant time between signing and closing” and a “[p]otentially significant breakup fee if transaction does not close”. An exhibit showing an internal Facebook “Q&A” outline on the WhatsApp deal flags a $2 billion breakup fee, representing 10.5% of the $19 billion deal value—a high percentage, as breakup fees tend to land more in the 2-7% range.

Who else but Morgan Stanley, the investment bank pushing for business, was WhatsApp’s financial advisor for the deal? Jim Goetz and his partners at Sequoia made out handsomely; their initial investments in WhatsApp of around $60 million in total would return over $3 billion from the buyout. The “bidding war” worked. Recall that it was stoked by an anonymously sourced, admitted “rumor” story in 2013 and a “happenstance” run-in between a WhatsApp employee that leaked the news to Facebook of a meeting with Google. Everybody who seemingly wanted a deal to happen—Zuckerberg, Sequoia, Morgan Stanley—profited. And all of it, from the valuation, to Sequoia’s investment, to the interest from outside bidders, to Facebook’s valuation and justification of the WhatsApp deal internally—seemed to explicitly or implicitly be based on the promise of WhatsApp monetizing, by using ads on other platforms as a comparable—exactly the strategy that WhatsApp’s founders didn’t want and Meta is now arguing in court today would have never happened.

Those are the broad strokes of where we are on the WhatsApp story—I have some more thoughts on individual witnesses further below. But before the day ended, the FTC turned back to Instagram to hear from the Sequoia Partner that led that investment, Roelof Botha, by video.

“Very High Possibility of Turning Into A Good Business”

The investment in Instagram that Botha led for Sequoia also moved at lightning speed. Botha reached out to Facebook to express interest. Then he wrote a “one-pager” summarizing the investment opportunity. Only one week later, he circulated his formal pitch memo recommending an investment and valuing Instagram at $500 million. When pressed about how he came up with these figures, Botha laughed, calling the process subjective—he all but admitted that he made the number up without doing any kind of discounted cash flow analysis, simply trying to avoid $1 billion because his partners would shoot him down for predicting a unicorn. He concluded that there was a “very high possibility of [Instagram] turning into a good business”. What started out as a “straight photo service” had ‘the potential to transform into something broader,” he testified. Botha’s investment philosophy is that “consumer services that succeed need to take advantage of one of man’s seven deadly sins.” Here, Instagram stoked vanity and pride, which would do. Botha pegged the “medium-term plan” for Instagram to expand “beyond photos into video expression and messaging.”

Botha wasn’t shy about his interest. He was “giddy” and “excited” about the prospect of investing in Instagram. “Wouldn’t you be?” he asked the FTC’s lawyer. “I don’t have that kind of money,” the government lawyer replied off-screen.

Trial continues Tuesday with Instagram co-founder Kevin Systrom due up.

Other Things

I didn’t find the FTC’s expert, Rim—the former Kakao CEO—all that effective. His testimony seemed designed to rebut Jim Goetz. But Rim’s testimony was so reliant on Sequoia docs and Goetz emails that he seemed to add little more than an opinion about how to weigh the evidence from fact witnesses. That’s a role for the factfinder. Sometimes expert reports or parts of them are stricken for merely being “ipse dixit” (meaning “because I said so,” in effect) or regurgitating the words of fact witnesses. Because the court can weigh the testimony itself, it doesn’t need an “expert” to offer their interpretation of the evidence.

Meta lawyer Alex Parkinson returned for a more muted performance on cross, casting all kinds of doubt about Rim’s credibility: accusing Rim of not disclosing his mixing and matching of U.S. and worldwide data (shown through different colored bars in a chart and disclosed in a footnote, the FTC pointed out); and of not using the FTC economist Hemphill’s third-party Comscore data which suggested lower time usage for Instagram back in March 2012; and then pulling up blog posts Rim wrote about this case and his role in it, unusual and not recommended for experts to be doing.

Some of the more effective sequences simply showed that Rim didn’t know much about the “24 potential investors” he flagged for WhatsApp on a slide, like Suhail Rivz[i] (which appeared incorrectly spelled with a “y”); didn’t know much about Hemphill’s data that he relied on (and didn’t read Hemphill’s report); and couldn’t cite any evidence about WhatsApp planning to expand into social networks. Chief Judge Boasberg looked thoroughly unhappy by the end of Rim’s testimony. But ultimately, the cross might have done more than it needed to do. Rim’s testimony doesn’t add that much affirmatively beyond the point that WhatsApp was losing $120M+ a year. Expect Chief Judge Boasberg not to place too much weight on it.

If Rim was the “because-I-say-so” witness of the day, Arora was the one who couldn’t remember. Chief Judge Boasberg was frustrated by the regular and repeated moves to refresh Arora’s recollection, at one point prompting the questioning attorney to simply ask the question in a more general way to avoid the need to refresh. The testimony has been pretty repetitive at this point. Expect the court to become more active in moving things along; it didn’t want more than 90 hours of trial time apiece, and the FTC wanted twice that for its case.

You get the strong impression from Sequoia Partner Roelof Botha that venture capital firms just wing it. He might as well have said the $500 million valuation was splitting the unicorn difference on a napkin. The Sequoia evidence makes it seem—more by the impression of the witnesses themselves than by anything spotlighted by Meta—like they carefully orchestrate bidding wars based on questionable comparables. And that’s part of Meta’s theme, that WhatsApp and Instagram were built up to be more than they were or could be without Meta.

One correction & update: My last entry originally stated that Meta wasn’t uploading defense exhibits; but at least one defense demonstrative appears to have been uploaded the day before that, and this is a joint repository governed by court order. The exhibits get uploaded by the producing party, so Meta has had to upload the FTC’s exhibits that Meta produced. After we last checked while getting ready to go to press, Meta uploaded more defense exhibits ahead of an 8pm deadline to do so. More were uploaded today. You can check them out here.

One of the better articles here to me on the Goggle and Meta trials. This one really exposes the games Wall St and Silicone Vally have been pulling off for the last 20-25 years. I think it was in the late 1990's with the "cable cowboy" John Malone really getting the "Growth stocks" phenomenon going. Value stocks? no growth is the way to go. My $10 stock will be $100 in 3 years. As the Wall St boys jumped in and basically did the new version of pump and dump. Except here they pumped these platforms up and sold them to each other in this group over and over. I mean, 20 years before Amazon even turns a profit? Really? New version more sophisticated way of doing pump and dumps like Joe Kennedy and his buddies did back in the 20's. Kennedy is looking down laughing his ass off.

This article is great at reflecting this scheme. And this has been done numerous and numerous times with these guys over the years.

Really helped too after the 07/08 crash and these guys got even more money to play these games. Plenty of juice in the system with all of the cheap easy money.

We need to return to value investing. It's honest and the truth.

Great read thank you.

https://www.simonandschuster.ca/books/No-Filter/Sarah-Frier/9781982126810

In the book "No Filter: The Inside Story of Instagram" writer Sarah Frier wrote that Mark Zuckerberg always wanted his baby "Facebook" app to be the top app at the company and prevented Instagram and Whatsapp from competing after he both them.

The whole book is filled with tons of great stuff for this case.

She writes all about it. Has anyone questioned her?