TikTok Is "Not A Social Network"

Meta's relentless focus on TikTok as a competitor blows up in Day 4 of FTC v. Meta trial. That's good for the FTC.

When the stakes are high in litigation, sometimes it’s tempting to throw in the towel early. And there are few cases with higher stakes than a breakup of a business—it’s bet your company. The stakes are high for the government, too: while there’s certainly merit to bringing “difficult cases” against anticompetitive conduct, there’s significant legal and political risk in devoting scarce resources to prosecuting an action that’s uncertain.

From expert witnesses to court reporters to giant servers hosting discovery materials, an antitrust case against a Big Tech company costs millions of dollars to prosecute. More than that, it’s very much a bet your reputation case for the trial team to convince the Commissioners a case is worth pursuing to the end. Having been in the trenches on both sides of major antitrust litigation, I can tell you how uncomfortable it can be to face clients with bad news while asking for their trust so that you can keep pursuing the truth of what actually happened and get them to the result they deserve.

These dynamics are all the more challenging in a saturated media environment. There is a bevy of reporters covering the FTC’s trial to break up Meta, and they are all working hard. But sometimes, for reasons of bias, not having legal training, or, as we’ll get to below, technical snafus, important threads in the trial may not get the airtime they deserve. And some aspects of trial get more airtime than they deserve—and that’s true of testimony that’s unhelpful for the FTC’s case from Meta’s own executives. What did people expect, that Sheryl Sandberg was going to testify that Meta is a criminal enterprise and all the company wanted to do was ruin competition? Don’t be naive. This mismatch can cause the court of public opinion to reach a verdict that’s different from the way the actual court will rule—and up the pressure on the enforcers to quit while they’re behind.

To put it bluntly: sometimes you have to get repeatedly punched in the face over the course of years of litigation before you finally start landing punches of your own.

The FTC landed its first major blow of its case to break up Meta in a little-covered deposition video that played just before the fourth day of trial closed. (So far as I’ve been able to find, only Law360’s Bryan Koenig (subscription required) covered this testimony.) After the court closed the courtroom and video feed to the media room for a sealed portion of questioning, presumably over YouTube’s “communities” feature, it opened back up again without restoring the video feed to broadcast testimony from perhaps the most important witness of trial to date: the former acting head and COO of TikTok, V. Pappas (they/them, she/her; I will use they/them).

For TikTok, Content—Not Social Networking—Is King

What makes TikTok so important? Over here at Big Tech on Trial, we’ve shown you how Meta’s opening statement and its questioning of Mark Zuckerberg put a spotlight on TikTok as the principal competitor to Meta. Whether TikTok is within or outside the relevant antitrust market will affect Meta’s market shares, and with it, the ability to show monopoly power. (Although, as we’ve also previewed, it’s not necessarily fatal to the FTC’s case even if TikTok is part of the relevant market.)

Meta’s Chief Legal Officer, Jennifer Newstead, said that “every 17-year-old in the world knows [that] Instagram competes with TikTok” among other apps. Here’s what Meta hoped to prove with TikTok, as shown from its opening statement:

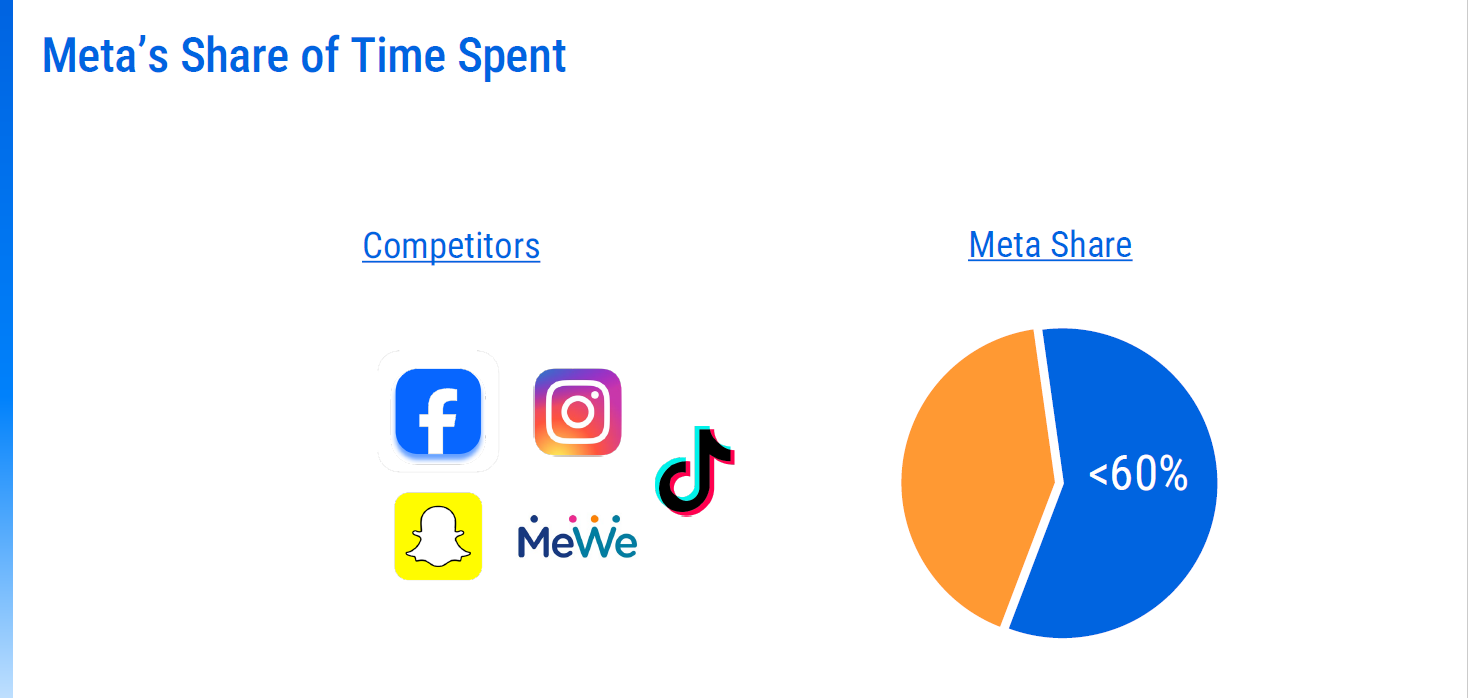

Facebook, Instagram, Snapchat, and MeWe together make up the FTC’s proposed “personal social networking services” (“PSN”) market. Without TikTok in the market, the FTC says that Meta’s market share is around 85%. With TikTok in the market, that market share falls to below 60%, as shown on the above slide—if “time spent” is an appropriate measure of market share.

Now at the outset, it’s not exactly clear that a market share of above 50% but below 65% dooms the FTC’s case. Sure, one way to make out a prima facie case of monopoly power involves a market share of 65%. But there are other cases out there that say that a market share of 50% is enough (and, theoretically, even below 50% in the rare case, or for attempted monopolization)—if accompanied by high “barriers to entry” that make it difficult for new competitors to get a foothold. And the FTC hopes to prove that those barriers are, in fact, very high. So, right out of the gates, if TikTok were the only other competitor inside the market, it may not end up mattering all that much.

Maybe every 17-year-old knows that TikTok competes with Meta, but one of the most important people didn’t know that, at least not in the way that matters for market definition: Pappas, who before becoming COO oversaw TikTok’s operations in the United States. The FTC played clips of their deposition in this case, and they put it bluntly: TikTok is “not a social network, primarily we’re an entertainment platform,” focused on “content first and foremost.” But Instagram “is a social network,” and Facebook is one, too, they testified.

While we’ve heard lots of testimony about how Meta’s apps are built around a “social graph,” Pappas testified that TikTok is “predicated on a content graph,” by contrast. They testified that Instagram has “focused on communications,” while TikTok saw itself playing in a “post-social network landscape,” as there were “no other products predicated on a content graph”. This difference also played out in how users actually use the apps—they “check” Facebook and Instagram, but they “watch” TikTok shorts. TikTok at one point experimented with a “friends” tab, but at the time of the deposition, was considering scrapping it altogether because it was “ancillary” and “hasn’t been an incredibly strong consumption” use-case for TikTok. TikTok saw itself competing with YouTube more than anything else, which makes sense, because Pappas spent seven-and-a-half years at YouTube.

That’s not to say this testimony was a slam dunk. Meta’s counsel got Pappas to say that TikTok “competes with Facebook, Instagram, Netflix, YouTube, and Amazon for time and attention,” but doesn’t “directly compete with Facebook for entertainment.” Pappas didn’t seem to be up to speed on Facebook Reels, showing that perhaps they lacked foundation for that statement. And Meta’s counsel used what appeared to be a sworn declaration from Pappas in litigation characterizing TikTok as “social media,” which they explained as simply “one categorization” for the app. Pappas, who left TikTok in 2023, is on Meta’s witness list to testify in person at trial. Perhaps things have now changed, and the testimony will, too. Apparently, depending on the user, the “friends” tab in TikTok still exists. And that’s part of why this case is going to trial. If either side had delivered a knockout blow, maybe we wouldn’t be here. But each side scored some points that help its case. It is often when the evidence is near equipoise (balance, equilibrium, etc.) that cases head to trial.

Even so, as I’ve argued here, “time and attention” isn’t the relevant question for market definition. Lots of things in the world compete on time and attention but aren’t direct competitors in a product market for antitrust purposes. And that’s part of what makes Meta’s “natural experiments”—premised on blackouts of apps—so silly. Netflix and reading a book aren’t competitors just because people might read by candlelight when the power goes out and they can’t watch Netflix. In the same way, TikTok doesn’t compete with Instagram and Facebook just because they are all things that you can waste time on on your phone or computer. Even if it’s true that they compete for time and attention, the point is that that competition may be insufficient to discipline or change Meta’s behavior on the core use-case of friends and family sharing. Meta launched short-form video as a product to compete with TikTok, but it’s hard to say that TikTok competes with “old” Facebook blue and its focus on profiles, posting on a friend’s wall, forming kickball groups, inviting people to BBQs, or throwing them a mysterious “poke.” As Pappas explained, “the magic of TikTok is the serendipity.”

Suddenly Sandberg

TikTok closed out day 4. But things started with a continuation of former Meta COO Sheryl Sandberg’s testimony, after she shivved the FTC in her charming way on day 3 (our recap of that here). Since witnesses are only called once, I’d describe Meta’s questioning at the end of day 3 as a cross of the FTC’s direct, and today’s testimony more like Meta’s own direct: we heard how Mark Zuckerberg hired Sandberg from Google to help build and grow the business with advertising, which she worked on at Google. Sandberg credited Facebook with helping millions of small businesses “around the world” grow “in a way that was different than before the internet.” Facebook had “time and attention,” which made advertising a natural path for revenue; “ad dollars track time spent.” The implication was that Meta can only monetize if the user experience is good; if users spend less time on their platforms, then Meta makes less money.

Facebook had an advantage over early Google search in ads because Facebook “[u]nderstood who people were and [could] serve them ads relevant to their interests,” which would particularly help small businesses. Of course, many have said that on Meta’s apps, the users are the products. But Zuckerberg and Sandberg describe Meta like Lake Wobegon, “where all the women are strong, all the men are good-looking, and all the children are above average.” In the Meta-verse, everything is always done with the best of intentions:

Sandberg got into how Meta targets ads based on users’ own “characteristics.” Steering clear of race, she said that they could target ads based on gender and location. It was surprising to see this spun as something positive as Facebook has been sued repeatedly for targeting ads based on protected characteristics; the Ninth Circuit, a federal appellate court, said that claims that Facebook’s targeting of housing ads based on race violated the Fair Housing Act could go forward. Meta claims that it stopped targeting ads based on race, but critics have pointed to using other proxies. Sandberg, for her part, says “everyone personalizes ads” now.

As with Zuckerberg, from here Sandberg started spouting the company line in a way that made Chief Judge Boasberg look skeptical. She said that Facebook wanted ads “to be as high quality or even better than the organic content” and that “[o]ver time, we achieved that.” Asked how she knew that users wanted to see ads, Sandberg answered: “Because they stopped and engaged with them.” Meta’s counsel next tried to preempt an argument we’ll hear from the FTC’s economist, Scott Hemphill, that Meta could in effect “price discriminate” by showing more ads to people who wanted to see more friends and family content. Sandberg admitted that Meta had “dynamic ad load,” a feature where they can change how many ads a particular user sees. But she was unequivocal that they don’t target based on friends and family sharing: “That’s not true and doesn’t make any sense.” Dynamic ad load targeting is “based on engagement or characteristics.”

At that point, Chief Judge Boasberg jumped in, explaining that from what he knew of Hemphill’s point from summary judgment, the argument was that users who like friends and family sharing are more captive to the network, and so the relevant question is, “did you take that into account when you decided ad load?” Sandberg testified that she didn’t “believe so.” And she’d “argue against the idea that friends and family users are captive” because “switching costs on a phone are very low”—a variation of the (in)famous Google line that competition is a click away. Chief Judge Boasberg said that might be “where it is now but may not have been the case a few years ago.” Sandberg countered that “friends and family sharing went way down over time,” and “if you had a strategy of targeting friends and family, you’d have serious revenue issues.”

Shoring up some other points, Meta’s lawyer showed a 2020 deck projecting that TikTok could put more than $5 billion in Meta revenue at risk in 2024, and Sandberg testified that that’s why Meta developed Reels. That made TikTok look more like it’s in the same market as Meta. Asked if Instagram could have built a successful ads business just as fast without Facebook, Sandberg said that was “false”: “We know because they tried.”

Susan Musser then came back for the FTC’s re-direct with an important clarification that caught the judge’s attention: while Sandberg said that friends and family sharing declined as a percentage of time spent on Instagram and Facebook, did she know that absolute friends and family time spent decreased? Sandberg said she didn’t know and that there was probably data the FTC could find on that.

It was an important point: If total time spent on the apps is increasing, but friends and family sharing time remains constant, it could mean users are paying a time tax from higher ad load to achieve the same usage of friends and family sharing they had before. That’s an anticompetitive effect, and it helps show that Meta can impose that tax without losing users, so is a monopolist. Musser then walked back Sandberg’s claims that users like ads, establishing that Sandberg had no foundation to make that claim because evaluating how ad load impacted user sentiment wasn’t part of her job.

All in all, an effective re-direct.

Masters of the Universe

Next up was Jim Goetz of Sequoia Capital, the famous Silicon Valley venture capital firm that was an early investor in WhatsApp. Having worked with investment banking and tech clients or had them as opposing parties, I found Jim Goetz to be pretty much the real deal: he’s a smart, no-nonsense guy (aside from one or two eyebrow-raising answers), with a lot of knowledge about the mobile industry at his fingertips. Here’s him giving a lecture about how often major disruptors and competitors (my words) start as small companies focused on solving a specific problem for a specific customer:

The FTC’s point in calling him was to show that WhatsApp could have branched out from a pure-play messaging app into a broader social networking super app that would challenge Facebook. And to show that WhatsApp had other potential backers so could survive without Meta. We looked at Goetz’s early pitch memos to his partners on the case for WhatsApp: it was unique because it didn’t have a lot of G&A, or general and administrative expenses, a financial term for overhead. A 2013 memo for the Series B round of funding noted that 53% of WhatsApp users are active on a daily basis and 76% on a monthly basis, which Goetz called “exceptional.” That analysis drew a distinction from Apple’s iMessage, which had “no multi-platform ambitions,” as Apple prefers to keep its walled garden and not make software available on other operating systems. That same memo said that “Facebook is the most significant threat given their user base,” and Goetz testified that he was likely referring to Facebook generally, not to Facebook messenger. As of April 2013, Sequoia had a 13% stake in WhatsApp. But this was the memo’s key line:

“Separately, with a global user network WhatsApp has the opportunity to build out a social platform either as a standalone company or via acquisition by an existing social player."

Sequoia’s valuation for WhatsApp used Facebook as a comparable for WhatsApp’s potential in mobile ads—even though the WhatsApp founders’ approach was “No ads! No games! No gimmicks!” This resulted in absolutely bonkers valuations based on what’s known as a multiple of EBITDA (earnings before interest, taxes, depreciation, and amortization). When I started my career a decade ago working on defense-side M&A litigation, an EBITDA multiple of 10x or 12.5x was considered the bluest of blue chip. But this memo had valuation scenarios using EBITDA multiples of 20x and 25x—unheard of.

The best document shown during the FTC’s direct of Goetz wasn’t admitted for its truth, but for its effect on Sequoia. It was a 2012 email from WhatsApp founder Jan Koum to Goetz, where Koum wrote:

"yeah talked about WeChat with Zuck on Sunday at length. he was actually very concerned Tencent was trying to buy us to compete with FB outside of china"

This is exactly the case the FTC is trying to make: Zuckerberg was concerned about WhatsApp because it had potential to follow WeChat’s lead and pivot from a standalone messaging app to a super app with social networking.

Goetz would seem like a home run for the FTC, but it wasn’t that simple. The issue, as Meta sees it, is how much WhatsApp’s founders wanted to pivot to social networking, vs. how much this was all sales speak from Goetz—using the potential that WhatsApp could become another Facebook to drive aggressive valuations to get other investors on board, which in turn would make Sequoia’s stake worth more. Chief Judge Boasberg at one point wasn’t buying it, asking what it mattered to Sequoia whether WhatsApp went public or had a private buyer, and while Goetz answered that there’s more growth opportunity in an IPO, he didn’t quite answer the court’s question. On cross, Goetz said that he wanted WhatsApp founders to pivot, but was “quickly shot down and dismissed.” There was “major risk” early on that WhatsApp would never make money, but Goetz’s confidence grew.

And that’s another reason we’re here at trial. Was WhatsApp a real nascent threat? Or was Sequoia just hoping that it would be to jack up the acquisition price? If there’s some way to admit that email about Koum’s conversation with Zuckerberg or substantiate what it says, that may be the most important takeaway.

“The Core Use Case of YouTube Is Watching Video.”

The FTC’s last live witness of the day was Aaron Filner of YouTube/Google. He started with a good line for their market definition: “The core use case of YouTube is watching video.” The FTC’s Musser walked him through some of YouTube’s functionality to draw distinctions with Meta’s apps: there is no way to tell which YouTube videos your friends have watched, liked, or commented on from the YouTube homepage feed; YouTube searches lead to particular videos or other search terms, not to accounts per se; there are no friends and family sharing features; YouTube channels don’t know who their subscribers are, unlike friends and followers on Meta apps; and YouTube ended its stories and direct messaging features.

On cross, Meta lawyer Alex Parkinson got Filner to agree that sharing of YouTube videos often happens off-platform or across platforms, or within the platform through publicly viewable playlists. Both Musser and Parkinson tried to use Google’s submissions to foreign antitrust regulators to argue that YouTube was or was not a social networking platform; but Filner answered definitively on cross that Google doesn’t group YouTube together with Facebook and Instagram as “social media players” outside of a slide Parkinson had up. Meta’s cross finished with YouTube “communities,” a feature that sounds more social as it allows creators and fans to send messages and interact. The court then closed to the public for a confidential session, which presumably kept up with this topic.

There are no trial days on Fridays. We’ll be back for the second week starting Monday.

Stray Thoughts

The exhibits are posted here, two days after they’re admitted in court. (Correction & Update: an earlier version of this piece stated that Meta wasn’t uploading defense exhibits; but one appears to have been uploaded yesterday, and this is a joint repository governed by court order. The exhibits get uploaded by the producing party, so Meta has had to upload the FTC’s exhibits that Meta produced. Since I last checked, Meta uploaded more defense exhibits ahead of an 8pm deadline to do so.)

Shout-out to the debaters. In college, I did something called “policy debate,” a form of competitive speech and debate that’s heavy on research and something called “spreading,” which is talking as fast as you possibly can to make as many arguments as you can within the time limit for your speech. Because the skillset is similar, policy debaters often go on to careers in the legal world. But this trial is unique for having a few debaters from the era I competed in as counsel to parties and non-parties. Meta’s lawyer questioning YouTube’s Filner was Alex Parkinson of Kellogg Hansen. He debated at Harvard a year ahead of me at Boston College, and his cross-examination of Filner named his “college friend Eli" in a hypothetical question—probably a reference to his debate partner, Eli Jacobs (now also a lawyer). They were a really good team, ranked second in the nation in 2011 ahead of the National Debate Tournament, which is like the playoffs of collegiate debate. Jacobs & Parkinson debated my partner and I that season, and we got our butts kicked. Parkinson hasn’t changed much; he still has an uber sarcastic, prep school villain persona that the press room was absolutely loving: one journalist called him their “favorite” lawyer they’d seen so far.

But he’s not the only debater in the case! His colleague at Kellogg Hansen, Ana Nikolic Paul, is also on the trial team and has been sitting at Meta’s counsel table regularly. She was a very fine debater in her own right as an undergrad at Emory and also ranked in the top 25 teams in 2011. Boston College was a big fan of her as a judge after she graduated. And John Karin of Wilson Sonsini, who debated for Cornell (also class of 2011), is counsel to Snap as a non-party. John Karin and I were colleagues at Cravath in New York, where we were joined for a time by Parkinson’s wife, Catalina (née Santos), now of Hogan Lovells—also a Harvard debater and lawyer. As you can gather, it’s a small and perhaps elitist/insular world, though I didn’t debate in high school, so spent college trying to catch up to these folks. It’s nice to see them doing well and entrusted with meaningful roles at trial.

One note on something we said earlier and have since corrected: it’s not clear that DST Global owned part of WhatsApp before Facebook acquired WhatsApp, even though DST’s Yuri Milner says that WhatsApp was a portfolio investment of theirs. The FTC has shown documents that DST Global was considering an investment in WhatsApp, and Goetz made it sound like Sequoia didn’t really want them at the table, since their interest came from an organic connection between Koum and Milner. And perhaps reading my mind or this blog, Mark Hansen got Zuckerberg to say that WhatsApp’s founders were its “controlling shareholders”—which doesn’t necessarily mean they had a majority ownership stake, rather than holding the majority of voting shares. We’ll have to get to Rahul Mehta of DST Global, who’s on the FTC’s witness list, to find out what their investment was exactly.

This was a truly excellent recap.

The media reference to a "favorite attorney" both paints a vivid portrait of the aptitude of journalists covering the trial and grates like nails on a chalkboard to those in the legal profession.

I realize “time spent” is used to measure market share because that is the metric used by ad buyers. But why? When magazines competed against television for a share of ad dollars, they would have loved if ad buyers had bought into that pitch. Because magazine readers spent more time with a magazine than TV viewers spent watching a :30 minute show. Ad buyers didn’t buy that pitch because TV reached more people per minute than magazines. It took time for magazines to build reach, because they relied on “pass-a-long” readership for a significant proportion of their reach.

In the early days of Social Media, their reach also took a long time to build, just like magazines. But Sheryl was able to convince ad buyers that “time spent” was valuable because TV reach per minute (around 33%, when there were three choices) had dropped significantly due to competition. Now, ironically, Social Media reach per minute now surpasses TV, as evidenced by how quickly visceral misinformation can go viral. That’s why reach per minute is the clearest metric for measuring whether there is competition in any media.